How a Chinese Company Lost Millions to a Fake Ethiopian Partner — Top 5 Red Flags When Partnering in Africa

How a Chinese Company Lost Millions to a Fake Ethiopian Partner — Top 5 Red Flags When Partnering in Africa

By Africa Risk Control – When foreign investors or international firms seek local partners in Africa, they often find valuable on-the-ground insight, connections and market access. But such partnerships come with risks. Here are five red flags to watch out for — with real cases to illustrate why due diligence matters.

1. Misrepresented Ownership or Beneficial Ownership

What to watch for:

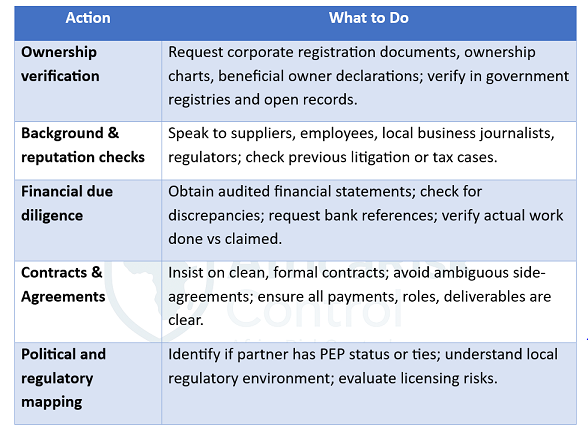

If the local partner claims ownership or control over assets but doesn’t have clean or transparent records (e.g. no registration documents, or the beneficial owners are hidden via family or offshore vehicles), it’s a major risk. It may be that the person you believe is the local partner is just a front for someone else, or that control can turn unexpectedly.

Case & Example:

In “Summary of Fraud and Corruption Cases in International Development Projects,” it’s common in Africa for local partner companies to be shell entities owned or controlled by relatives of government officials or even public servants. In many cases, all the work is done by the foreign company, but the “local partner” takes a fixed percentage (sometimes as a conduit for bribes).

The Simandou mining rights case involving Beny Steinmetz (in Guinea) showed that documents were forged and beneficial ownership obscured in order to win rights and mislead co-venture partners or the state.

s-rminform.com

Why this matters:

Hidden ownership can bring sudden liabilities: regulatory, political (if the owner is a PEP or under sanction), or reputation damage. Also, distributions of profits may not follow what was agreed once true control is revealed.

2. Demands for Side Agreements or Middlemen

What to watch for:

When you’re told you’ll need a “side agreement” (outside the official contract), or payments through middlemen / local agents with vague roles, that’s often an early sign of hidden payments, corruption, or attempts to launder deals.

Case & Example:

In a case cited in Addressing corporate fraud and corruption in Africa, foreign companies bidding for infrastructure or state contracts were told that after winning, they must pay an opaque “third party vendor” or middleman “for assistance” even though that party has no visible role. The foreign company attempts due diligence, but access to information on that third party is obstructed.

The McKinsey & Company Africa case: in resolving a bribery scheme involving state contracts in South Africa, part of the practice was working with local partners or intermediaries in ways that obscured payments to officials. Contract awards were influenced via these intermediaries.

Why this matters:

Side agreements often violate local and international laws (like FCPA, UK Bribery Act). They leave the foreign investor exposed to legal penalties, reputational harm, and unpredictable risk if the middleman is a weak link or becomes a liability.

3. Lack of Financial Transparency or Audited Financials

What to watch for:

Local partner cannot/did not produce audited statements; financials are outdated, prepared internally without external verification; discrepancies in financial claims vs reality; heavy use of cash, untraceable transactions, or transfers to offshore accounts.

Case & Example:

Fraud and Corruption Cases in International Development Projects, false invoices and fictitious cost claims are often made by local partners. In one instance, a contract required a local partner to do 25% of the work, but in practice, they were a “front” (i.e. the foreign party did much more). Payments were diverted.

In the red flag bulletin “Guinea: Swiss court convicts mining magnate of bribery and forgery,” Steinmetz was convicted partly for forging documents tied to mining rights and misrepresenting financials during joint venture negotiations.

Why this matters:

If financials are opaque, you cannot properly assess profitability, liabilities (debts, liabilities not shown), or tax exposure. Also, lack of proper audits increases risk of fraud, misallocation of funds, or undisclosed obligations.

4. Weak Local Reputation & Disputes

What to watch for:

Check local sources — media, suppliers, employees, regulators. If there are unpaid supplier debts, tax disputes, local lawsuits, reputation for delays or non-performance, this can indicate future risk.

Case & Example:

In “10 Red Flags We Uncover in Ghana During Due Diligence Investigations,” one of the red flags is local reputation damage: companies that look clean on paper but are known locally for damaging the environment, ties with illegal gold miners, not paying workers, or tax issues.

The PwC example: PwC is exiting more than a dozen countries in Francophone Africa because some of its local member firms couldn’t meet global compliance / client risk standards, or because reputational risk from local partners was too high.

Why this matters:

Reputation issues can delay projects, lead to legal claims, affect permits, or cause public backlash. What looks like a small problem may escalate and drag in the foreign partner by association.

5. Political Exposure and Regulatory Risk

What to watch for:

Local partners who are Politically Exposed Persons (PEPs), or who have close ties to current politicians, or who are involved in lobbying/regulatory capture. Also, frequent changes in regulation, requirement of special licensing, hidden requirement for approvals.

Case & Example:

The Bolloré group case (ports, concessions) is illustrative: the group has been accused of obtaining port and infrastructure concessions through relationships with political elites in countries like Togo, Guinea, Ivory Coast, and Cameroon. These political ties have led to accusations of corruption, legal claims, and regulatory scrutiny.

The McKinsey & Company Africa case: part of the problem was that contracts were awarded in politically influenced state-controlled entities (Eskom, Transnet) in South Africa. Knowing who the decision makers are and whether they are politically exposed is crucial.

Why this matters:

If your partner is politically exposed, potential consequences include risk of sanctions, regulatory investigations, shifts in politics that cut them off, or public scandal. Foreign investors are often held accountable under laws around anti-corruption and must demonstrate they did due diligence.

6. Fake Agency and Credit Fraud Schemes — The “Trusted Agent” Trap

What to watch for:

Some local representatives or “exclusive agents” open offices in foreign trade hubs such as Guangzhou, Dubai, or Istanbul, claiming to represent major African buyers or serve as distributors. They present themselves as trustworthy middlemen who can help foreign manufacturers reach African markets. But in reality, some use these arrangements to exploit weak verification processes and cross-border legal loopholes.

Case in Point – The Ethiopia–China Trade Scam:

A few years ago, a Chinese supplier extended millions of dollars’ worth of merchandise on credit to an Ethiopian businessman who had opened an “agent office” in Guangzhou, China. The Ethiopian presented himself as a well-connected importer with strong business ties in Addis Ababa’s wholesale markets. He used convincing trade documents and photos of a supposed warehouse operation in Ethiopia to win the supplier’s trust.

The supplier shipped several large consignments on open credit, expecting payment after resale in Ethiopia. But once the goods were distributed to local wholesalers, the “agent” found himself unable to collect the payments and vanished — fleeing back to Ethiopia.

Weeks later, Chinese merchants who had been defrauded traveled to Addis Ababa in search of him. In a rare display of frustration, they posted his photographs around the city’s main market district, warning others and seeking any leads to recover their losses. The man had, however, disappeared — leaving unpaid debts and a trail of forged contracts behind.

Why this matters:

This case highlights how easily cross-border fraud can occur when suppliers skip independent due diligence. A simple verification of the agent’s Ethiopian trade registration, background checks of the individuals business history, tax filings, and import records would have revealed that his “company” had no genuine business history. It also underscores how enforcement is extremely difficult once a fraudulent agent crosses jurisdictions.

In conclusion, partnering with a local company in Africa can unlock many advantages — market access, cost efficiencies, local knowledge. But without rigorous due diligence by experts, what seems like a good partnership can turn into legal, reputational or financial risk.

When you see several of these red flags together — non-transparent ownership, middlemen, dubious financials, weak reputation, political ties — treat them as warnings, slow down, escalate the checks, or consider alternative partners.