Foreign investment sentiment toward Africa has improved materially over the last 18 months, but Egypt is the market where capital is currently concentrating most decisively—not only because of mega real-estate and infrastructure flows, but because the country is becoming a regional energy-transition hub.

Foreign investment sentiment toward Africa has improved materially over the last 18 months, but Egypt is the market where capital is currently concentrating most decisively—not only because of mega real-estate and infrastructure flows, but because the country is becoming a regional energy-transition hub.

UN Trade and Development (UNCTAD) highlights that Africa’s 2024 FDI jump was strongly influenced by a major project in Egypt, and even excluding that one transaction, the continent still showed positive momentum.

For foreign investors, the core Egypt story is not “headline FDI” alone. It is that the state is prioritizing large, grid-connected renewables, accelerated permitting in strategic corridors, and—critically—export-linked “power-to-X” pathways that can turn Egypt’s geography and infrastructure into a tradable decarbonization advantage.

Why this sector is investable: three fundamentals

1) Execution and scale are already visible

The renewables narrative is not theoretical. Major international developers are building at scale, and projects are reaching completion faster than many comparable markets. Reuters reported Engie’s completion of a 650MW wind project on the Red Sea—an execution signal that global investors use as a proxy for bankability and administrative throughput.

Reuters

2) Export adjacency: power-to-X is the prize

Green hydrogen/green ammonia economics remain challenging globally, but Egypt’s value proposition is clear: proximity to European and Middle Eastern offtakers, Suez-linked logistics, and the ability to integrate renewables, ports, and industrial zones into an export system. Investors that treat hydrogen as an “announcement sector” will lose time and capital. Investors that treat it as an infrastructure-and-offtake structuring exercise can build optionality.

3) Macro backstop matters for project finance

FDI mega-deals (notably Ras El-Hekma) are relevant because they influence liquidity perceptions, sovereign risk pricing, and the confidence of lenders underwriting long-duration cash flows. Reuters reported the $35bn UAE-linked investment package for the north coast, and UNCTAD commentary identifies the Egypt mega-project effect in Africa’s 2024 FDI numbers.

Key investment opportunities (where foreign investors are actually deploying)

- Utility-scale wind and solar (IPP model and hybridization)

Egypt’s near-term “bread and butter” remains grid-connected wind/solar, increasingly paired with storage to smooth dispatch and improve revenue certainty. Foreign sponsors should look for: grid-strength corridors, curtailment risk allocation, and hard, enforceable payment mechanics. - Grid, transmission and balancing infrastructure

The fastest way to strand renewable capacity is to outrun the grid. Investors who can finance or co-develop transmission upgrades, substations, and balancing capacity can secure preferential positioning—especially when tied to large industrial offtakers. - Green ammonia/hydrogen export ecosystems (selective, phased)

The investable path is typically phased: (a) renewables scale-up, (b) contracted offtake with credible counterparties, (c) port/logistics integration, and (d) only then large electrolyzer deployment. “Big-bang” hydrogen capex without disciplined phasing is the dominant failure pattern globally. - Industrial decarbonization PPAs (private offtake)

Where grid risk or tariff complexity creates uncertainty, structured PPAs with industrial clients can improve predictability—if credit risk and convertibility issues are addressed contractually.

Major players in key segments

Global utilities/developers scaling wind and solar portfolios in Egypt (e.g., Engie and consortium partners on major wind build-out).

Reuters

Gulf sovereign-linked capital shaping the broader investment climate and liquidity narrative through large-ticket commitments (Ras El-Hekma is the flagship reference point in FDI discussions).

Local EPC and infrastructure groups partnering with international sponsors to execute and localize delivery (critical for cost control, interfaces, and government coordination).

Reuters

Risks & challenges

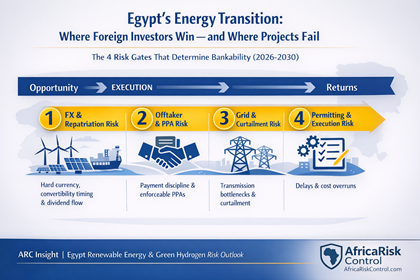

- FX convertibility and repatriation risk

Even when a project is profitable in local terms, hard-currency conversion constraints can disrupt dividend and debt service schedules. In Egypt, FX risk is not merely financial—it is operational (import cycles, spare parts, and EPC claims). - Offtaker/payment risk and contractual enforceability

IPP projects rise and fall on payment discipline and dispute resolution realities. Investors must diligence: the offtaker’s payment history, security package, escrow mechanics, and enforceability under stress. - Grid congestion and curtailment risk

Rapid capacity build-out can outpace transmission readiness. Curtailment allocation in the PPA is not a “lawyer detail”—it is a core driver of equity returns. - Policy volatility and permitting friction (sector-specific)

Even with strong political will, administrative processes can shift. The risk is not “no permits”—it is changing timelines, changing interpretations, or informal bottlenecks that create cost escalation. - Green hydrogen hype risk (timeline and price realism)

Hydrogen project announcements can be plentiful; bankable projects are fewer. The main risk is mispricing the timeline to final investment decision and underestimating offtake conditionality.

ARC risk mitigation strategies (practical, investor-grade)

- Structure FX and payment defenses upfront: hard-currency indexed revenue where possible, escrow or reserve accounts, step-in rights, and lender-friendly cure periods.

- Prioritize “grid reality due diligence”: substation capacity, interconnection queue position, curtailment history, and transmission upgrade commitments with clear milestones.

- Phase hydrogen exposure: commit first to renewables and logistics readiness; scale electrolyzers only after credible offtake and financeability are confirmed.

- Deep partner and contractor diligence: EPC track record, claims history, political exposure screening, beneficial ownership, and litigation checks.

- Scenario planning for sovereign stress: model delayed payments, FX tightening, and procurement disruption; pre-negotiate remedies rather than litigate under pressure.

Bottom line

Egypt’s renewables and green hydrogen stack is one of the most investable Africa themes right now because scale, execution, and geopolitical capital are converging. But the winners will be investors who treat this as a risk-structured infrastructure play, not a headline trade. The margin is made (or lost) in FX architecture, grid diligence, offtake enforceability, and contractor discipline.

If you are evaluating Egypt energy exposure (renewables, storage, or hydrogen-linked infrastructure), ARC can provide field-verified counterparty checks, grid/policy risk mapping, and bankability red-flag screening before you commit capital.